Heading off to college is an exciting journey, but as college costs continue to rise, figuring out how to pay for it can be overwhelming. With some planning and smart strategy, you can cross financing college off your list, and focus on what matters: your education.

Flickr user sea turtle

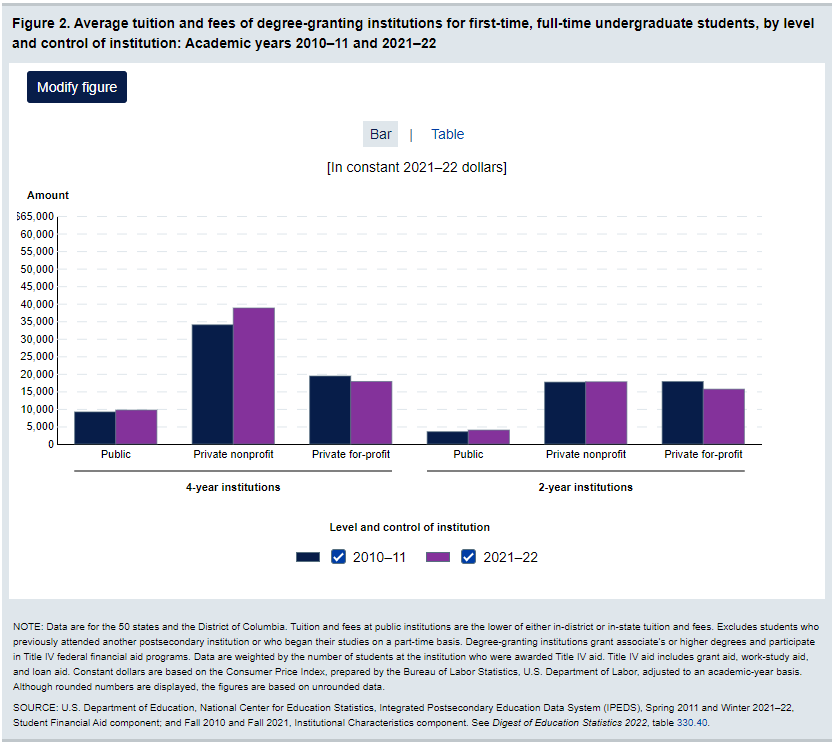

College Costs to Consider (and Ways to Save)

First, let’s discuss some of the new costs you’ll come across in college, and how you can save on those costs, reducing your financial burden. The overall cost of college is usually considered to include tuition, books and other supplies, and room and board. These costs varied widely depending on if you went to a public or private university or a 4-year or 2-year school. For example: in the 2021-22 academic year, the overall average cost of attending college at a 4-year public university was $9,700; however, to attend a 2-year private-for profit school was $15,600.

Image courtesy of NCES.

Tuition

The big one. Tuition fees can vary widely depending on the institution and program. Researching the average tuition costs of different colleges and universities that you’re interested in can help you plan ahead and make the best decision to pay for your tuition fees and education.

Room & Board

Consider where you’ll live during your college years and factor in the costs of housing and meals. Will you live on-campus, off-campus, or at home? Explore housing options, such as dormitories, apartments, or off-campus housing, and compare their costs.

How much will it cost? This depends on location and living arrangements. Calculate monthly rent, utilities, and food expenses to estimate your total room and board costs. Universities with dormitories also provide dining and various meal plan options, so check with your prospective schools’ Housing and Dining division for costs.

BONUS TIP: Most accommodations – including dormitories and apartments, require you to pay for laundry with coins or through buying tokens. Start saving those quarters now!

Books & Supplies

Don’t overlook the expenses associated with textbooks, lab materials, and other supplies. These costs can add up quickly, so plan for them. And look for ways to save, such as buying used books or renting textbooks when possible.

How to Pay for College

Once you’ve determined your costs for college, it’s time to figure out how to pay for it. The great news is that there are many options, and not all of them involve borrowing money – so you can be smart about how much to borrow and develop a mixed plan to pay for college that suits your needs – hopefully lowering your net price of college.

PRO TIP: Federal Financial Assistance requires filling out the FAFSA each year. Filling out this form will help schools determine some of your options for how to pay for college including federal grants, work-study programs and federal loans.

1. Free Money First: Scholarships and Grants

Scholarships and grants are valuable sources of funding that don’t need to be repaid. Research and apply for as many scholarships and grants as possible to help offset tuition and other expenses.

Scholarships are awarded based on various criteria, such as academic achievement, athletic ability, or community involvement. Search for scholarships with our free tool, and get on your way to funding your education!

Grants are typically need- or merit-based funds that don’t require repayment. They are awarded by the government, colleges, or private organizations to help students cover educational expenses.

Remember, not all scholarships and grants cover all costs outside of tuition, like books or room and board. Be aware that some scholarships and grants may only cover tuition or specific expenses, so it’s essential to read the terms and conditions carefully.

2. Earn While You Learn: Work-Study and Part-Time Jobs

Working while attending school means you’ll be busy, but it also could lower the financial weight on your shoulders, and help you gain valuable skills along the way. Consider participating in work-study programs or finding part-time employment to earn money to help pay for college.

Work-study jobs are wide ranging from library assistants to research aides and serving in cafeterias or watering greenhouses. These programs offer students opportunities for part-time employment on campus or with approved off-campus employers. To apply for work-study, fill out the FAFSA and begin searching at your school for job opportunities. These jobs work closely with the university and with your schedule.

Part-time jobs are another great way to earn extra money while attending school. Just be sure to be transparent with your new employer about your priorities, how much you’re able to work and your schedule. Check with your college’s career center or online job boards for available work-study positions or part-time job opportunities in your area.

3. Pay It Forward: 529 Plans and Savings Plans

Start saving for college early by investing in a 529 savings plan or setting up a private savings account specifically for educational expenses. Start saving for college early to maximize your saving potential and set yourself up for a stress-free education.

A 529 savings plan is a tax-advantaged investment account designed to help families save for future education costs by saving for college (pre-tax) while the child is growing, then withdrawing funds during college years.

4. Start Smart: Community College and Transferring Credits

Explore cost-effective options such as attending community college for the first two years before transferring to a 4-year university.

Community colleges often have lower tuition rates compared to 4-year universities. In fact, based on the cost research mentioned above, a public 2-year program costs almost 60% less than a public 4-year program. If you’re undecided about what career or major you want to study, getting your general education credits at a community college may be an economical option for you. Many colleges offer transfer programs that guarantee admission to a 4-year institution after completing an associate degree at a community college.

A great way to save on tuition costs (that requires some planning ahead) is to take High school courses that can count towards college credits. Take advantage of Advanced Placement (AP) courses in high school to earn college credits and reduce the number of courses needed to graduate from college.

5. Break It Down: Payment Plans

Many colleges offer flexible payment plans that allow students to spread out tuition payments over the course of a semester or academic year. Check with your college’s financial aid office or student services department for information on available payment plans and eligibility requirements.

6. Borrow Wisely: Federal & Private Student Loans

Consider federal student loans to cover remaining expenses after exhausting scholarships, grants, and other sources of funding. Through the FAFSA application and private student loans, you’ll find the funds to cover the remaining educational costs.

Federal student loans offer lower (usually) fixed interest rates and flexible repayment options, making them a more affordable borrowing option for many students. Apply for federal student loans in a few easy steps. Private student loans are also available depending on your program.

Another option worth considering if it is available, is borrowing from a family member. It is important with these loans to have very clear terms and trust established. They may offer favorable loan terms and repayment options. Just be sure that all parties are aligned with the terms and that they are documented.

Figuring out how to pay for college can be challenging, but it shouldn’t stop you from pursuing your goals. With the right plan in place, you can focus on what really matters—your education and future. By understanding the costs involved and exploring funding options, you can make informed decisions and a smart strategy.

Compare your Financial Aid Offers quickly and easily with our FREE tool! Or if you’re just starting your journey and looking for economical solutions, check out our ranking of the Top 25 Most Affordable Colleges.

This content is intended for informational purposes only. It does not take into account each individuals financial situation and should not be construed as advice. Please consult with your personal advisor regarding your own financial situation.