Roth IRAs and 529s are two types of tax-friendly accounts that can help families save for college tuition. As with any other type of saving program, neither one is best for all families, and both offer great benefits. Each has its own downsides too. Understanding the fundamentals of Roth vs. 529 can help you decide which one is a better fit for you (maybe it’s both).

How The Roth IRA Works & Its Pros and Cons

Originally designed as a retirement plan, the Roth IRA can also be used to save towards college.

With this plan, you can withdraw the principal portion tax free and penalty free and use it for any purpose after you reach the age of retirement. Withdrawing it prematurely can attract income tax and penalty unless the funds are withdrawn to pay for qualified higher education expenses.

There are income and contribution limits for this plan. As of 2021, married couples earning less than $198,000 can contribute a maximum amount of $6,000 to a Roth IRA account. Couples earning an income of $208,000 or more are not eligible to hold a Roth account.

Pros of Roth IRA

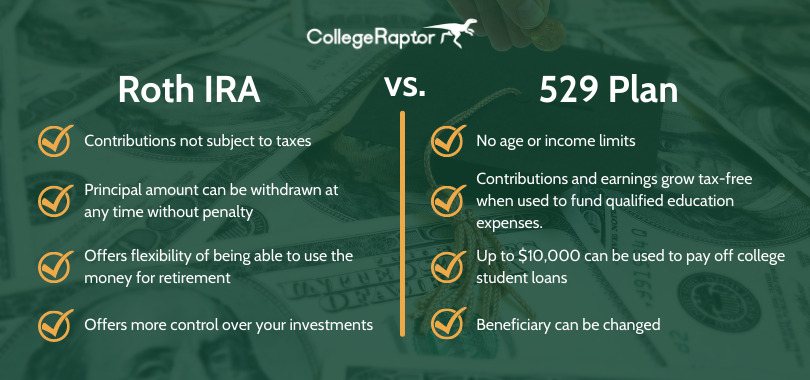

- Contributions and earnings are not subject to taxes.

- Contributions or principal amount can be withdrawn at any time without penalty or income tax.

- When the account holder turns 59 years 6 months, all the money – principal and interest – can be withdrawn without penalty or taxes, to help with children’s education expenses.

- Whatever money is remaining in the account can remain in the Roth to fund the account holder’s retirement.

Cons of Roth IRA

- Couples earning more than a certain income cannot contribute to the Roth IRA.

- The annual income and contribution limits can restrict your savings potential.

- For financial aid purposes, Roth withdrawals count as income. This can lower the amount of aid offered.

- You’ll still owe income tax on the earnings you withdraw to pay for college expenses.

- Using Roth savings for college reduces your retirement funds, which would have otherwise been tax free if withdrawn after retirement age.

How A 529 College Savings Plan Works & Its Pros and Cons

With a 529 account, there are no age, income or annual contribution limits. Neither is there any minimum contribution amount. You can open an account with as little as $25. Later you can adjust your contributions according to your finances at the time.

529 accounts are set up by the state and every state sets their own requirements and terms. You don’t necessarily have to open a 529 account in your state of residence. You can open an account in any state that’s offering better benefits.

There are two types of 529 plans. Savings plans, which are tax-advantaged savings accounts and Prepaid Tuition plans, allow you to pay the tuition fees in advance at specific colleges.

If the funds are not used for the designated beneficiary’s education, another beneficiary from can be chosen from among a specific list of family members.

Pros of 529 Plans

- There are no age or income limits but to avoid federal gift tax you’ll need to limit your annual contribution to $15,000 per beneficiary.

- Contributions and earnings grow tax-free provided they are used to fund qualified education expenses. These include college tuition, fees, room and board, $10,000 in student loan repayments, and up to $10,000 per year in K12 tuition.

- The beneficiary can be changed if the original beneficiary doesn’t use the funds to pay for higher education.

- Some of the money, up to $10,000, can be used to pay off college student loans.

- A 529 plan can be started with as little as $25.

- This is a largely a set-it-and-forget-it investment model where you just put the money in and watch it grow. The low starter funds and easy investment model makes it easy for anyone to get started.

Cons of 529 Plans

- Limited Investment options. Because every state offers different terms and benefits on their 529 plans, you’ll have to check plans carefully to choose one that’s performing well.

- You’ll pay taxes if the money is not used for the education expenses specified in the plan’s terms. In addition, you pay a 10% penalty to take the money back.

- Plans are limited to one beneficiary at a time. Families with more than one child will have to open multiple 529 plans.

- Significant 529 assets could reduce financial aid for the college student.

Roth vs 529: Key Takeaways

A Roth IRA may be the better college savings option for you if:

- You want the flexibility of being able to use the money for your retirement.

- There’s some uncertainty about your child attending college and there’s no other family member who plans to attend either. In this case, the money will automatically go into your retirement fund.

- You like to have more control over your investments.

A 529 may be the better college savings option for you if:

- You want to contribute more than a Roth IRA allows per year.

- You want the flexibility of being able to switch beneficiaries if your child chooses not to go to college.

- You’d like a savings account that family members and friends can contribute to.

- Your higher income disqualifies you from contributing to a Roth IRA.

Roth vs 529 plans aren’t your only options. Learn more about different types of saving plans and consider using our Financial Planner Tool today.