There are students who think they’re won’t get financial aid from the federal government. Therefore, they sometimes don’t see the point in filing the FAFSA (Free Application for Federal Student Aid). However, these students don’t realize that they may be missing out on grants and scholarships from their college. They’re even missing out on low-interest-rate federal student loans. Even families making more than $100,000 should still fill out the FAFSA.

Unless you are planning to pay full sticker price out of pocket for college (and you don’t mind), it is almost always a good idea to fill out the FAFSA.

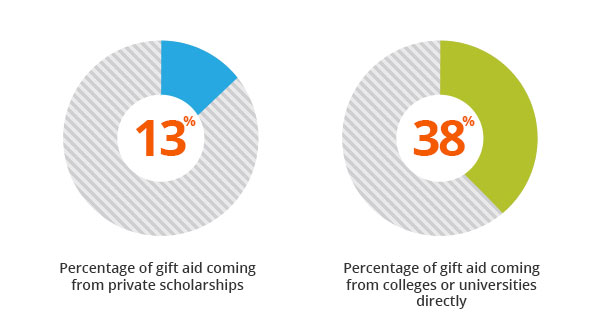

The FAFSA isn’t just used by the federal government

Many colleges, especially private ones, offer need-based grants and scholarships called institutional gift aid. This is on top of what the federal government offers. Different colleges offer varying gift aid, and colleges award the most aid to middle-class families. That doesn’t mean that students in other financial classes can’t or won’t get gift aid though. As long as you file the FAFSA, you have a chance of getting some form of gift aid.

Most institutions use the FAFSA to determine your eligibility for institutional need-based aid. If you don’t file the FAFSA, you could be paying thousands more for college than needed.

The US Department of Education offers more than just grant funds

Government aid programs only consider giving aid to students who filed the FAFSA. That includes federal student loans and work-study programs available to students from families with all ranges of income.

Federal student loans are often much cheaper than private student loans. Not only do federal loans generally have lower interest rates, but most also have a six-month payment grace period, and some don’t begin accruing interest until after graduation. If you have to take out a student loan, try to take out federal loans. Private loans are a last resort because they usually have higher interest rates and fewer repayment benefits and plans.

The US government also funds the Federal Work-Study Program. If work-study is part of your financial aid package, the government subsidizes part of your wages at a part-time campus job. Jobs vary from campus to campus, but there’s a wide variety of jobs available. From library assistant to IT support, you’ll most likely find a work-study job that suits your interests.

State governments also use the FAFSA to determine your eligibility for state-level financial aid. Most states have at least one grant or scholarship program available to in-state students who qualify.

The FAFSA should be refiled each year for College University aid

If you weren’t eligible for aid in the past, consider filing the FAFSA again anyway–especially if your situation has changed. If you have a sibling entering college, or if your parents’ marital or employment status has changed, you may now qualify for financial aid. There’s no harm in filing the FAFSA (besides taking up some of your time). Opening the door to more potential aid that you don’t have to pay back is always a good thing.

| Lender | Rates (APR) | Eligibility | |

|---|---|---|---|

|

|

5.99%-16.61%* Variable

4.24%-15.61%* Fixed

|

Undergraduate and Graduate

|

VISIT CITIZENS |

|

|

5.37% - 15.70% Variable

3.99% - 15.49% Fixed

|

Undergraduate and Graduate

|

VISIT SALLIE MAE |

|

|

5.37% - 17.99% Variable

3.79% - 17.99% Fixed

|

Undergraduate and Graduate

|

VISIT CREDIBLE |

|

|

5.98% - 13.74% Variable

3.99% - 12.61% Fixed

|

Undergraduate and Graduate

|

VISIT LENDKEY |

|

|

5.99% - 15.85% Variable

3.79% - 15.41% Fixed

|

Undergraduate and Graduate

|

VISIT ASCENT |

|

|

3.70% - 8.75% Fixed

|

Undergraduate and Graduate

|

VISIT ISL |

|

|

5.62% - 16.85% Variable

4.17% - 16.49% Fixed

|

Undergraduate and Graduate

|

VISIT EARNEST |

|

|

6.00% - 14.22% Variable

4.50% - 14.22% Fixed

|

Undergraduate and Graduate

|

VISIT ELFI |